Introduction:

The Indian startup ecosystem is thriving, driven by innovative entrepreneurs and supported by investors, accelerators, and incubators. From the early groundwork of pre-seed to the high-stakes expansion in Series A and beyond, understanding the objectives at each stage is vital for sustainable growth and success.

Image Source: https://inc42.com/reports/indias-top-200-startups-financial-index-report-2023/

Seed Stage:

- At the pre-seed stage, startups focus on developing a solid business concept, working on partnership agreements, obtaining patents or copyrights, and creating a compelling pitch deck. The emphasis is on laying the groundwork for the business idea.

- Once the pre-seed stage is completed, the seed stage follows. Here, the startup moves forward with creating a product or prototype based on the established business concept. The objective is to raise initial funds and get the business up and running.

- Funding Sources in Seed Stage: Self, family and friends, Micro VCs.

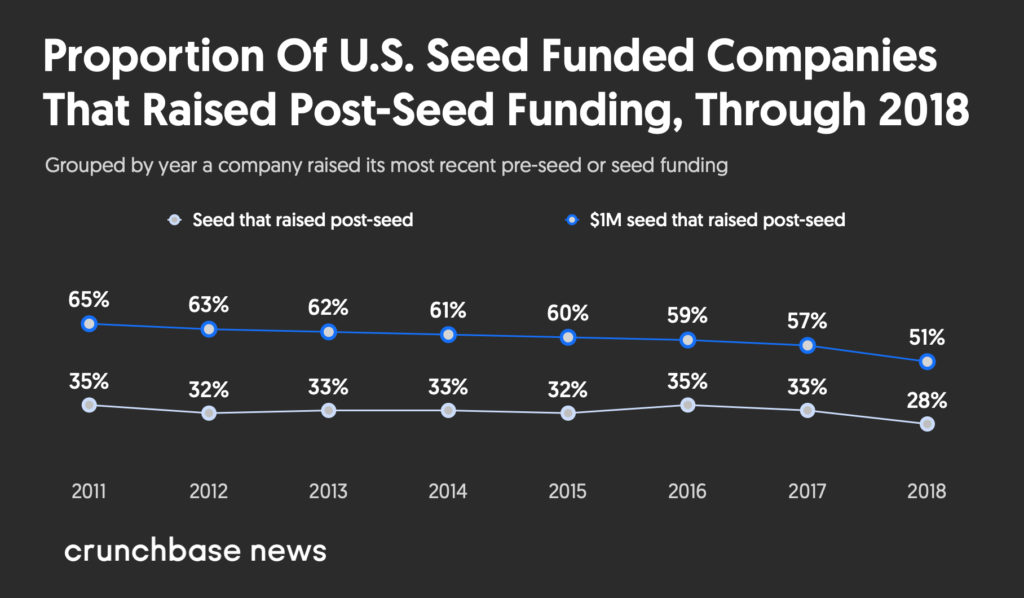

- But unfortunately, only 1 out of 3 startups successfully pass on to the Series A funding stage.

- At this stage, startups may encounter failure due to financial constraints and an improper product-market fit among other reasons.

Data Source: Why Fewer Than 1 In 3 Seed-funded Indian Startups Get Series A Funding – Forbes India

Image Source: What Are The Odds Of Success For A US Seed Funded Startup? (crunchbase.com)

Series A:

This stage involves-

- Researching industry and markets to identify growth opportunities.

- Writing a comprehensive business plan to outline strategies for expansion.

- Launching marketing and advertising efforts to gain customer traction.

- Generating revenue and aiming for profitability.

- Planning to scale into new markets.

- Funding Sources: Accelerators, Super angel investors, Venture capitalists.

Series B:

In Series B, startups focus on-

- Expanding consumer interest and market presence.

- Establishing a commercially viable product or service for scalability.

- Scaling production, marketing, and sales to meet growing demand.

- Funding Sources: Venture capitalists, Late-stage venture capitalists.

Series C & beyond:

In this stage, the startups concentrate on-

- Continuously innovating by building new products and exploring new markets.

- Establishing a strong position in the industry.

- Attracting investments from venture capitalists and late-stage venture capitalists for substantial growth.

- Funding Sources: Late-stage venture capitalists, Private equity firms, Hedge funds, and Banks.

Exit:

- Making an initial public offering (IPO) to offer shares to the public and provide liquidity to investors becomes a potential exit strategy.

- An exit through a sale or via VCs or SPACs is another way for investors and founders to realize the value of their investments.

Conclusion:

Startups not only create jobs and spur technological advancements but also disrupt traditional industries, fostering competition and pushing boundaries. Startups play a pivotal role in shaping economies, driving prosperity, and shaping the future. From Pre-Seed to Exit, the lifecycle of a startup represents an exciting journey filled with challenges, breakthroughs, and transformative impact.

Read more about Indian Startups: The Fast Track to Funding Your Startup: Convertible Notes, CCD, CCPS, SAFE

Expense Ratio

Expense Ratio